Average True Range Percentage

:max_bytes(150000):strip_icc()/ATR-5c535f8fc9e77c000102b6b1.png)

Average True Range Atr Definition

What Is Average True Range Fidelity

Average True Range Atr Chartschool

How To Use Average True Range True Trading Strategies Average

Moving Average Strategies For Forex Trading

True Strength Index Tsi Technical Indicators Indicators And Signals Tradingview

Average true range atr is the average of true ranges over the specified period.

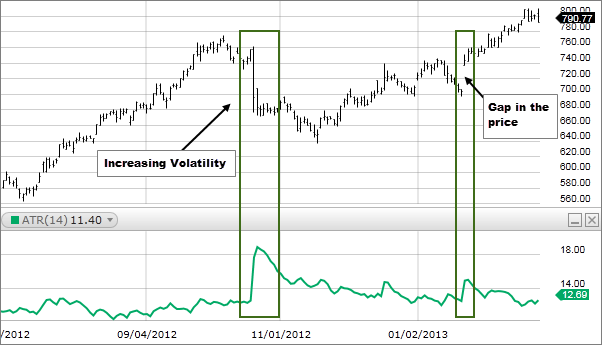

Average true range percentage. As is it average true range of an instrument can be easily compared to any other because of absolute percentage variation and not prices itselves. The average true range percent is the classical atr indicator normalized to be bounded to oscillate between 0 and 100 percent of recent price variation. Atrp allows securities to be compared where atr does not. Atr measures volatility taking into account any gaps in the price movement.

How this indicator works. Typically the atr calculation is based on 14 periods which can be intraday daily weekly or monthly. Atrp is used to measure volatility just as the average true range atr indicator is. To measure recent volatility use a shorter average such as 2 to 10 periods.

Usually the average true range atr is based on 14 periods and can be calculated on an intraday daily weekly or monthly basis. Average true range atr is a technical indicator measuring market volatility. Atr measures volatility taking into account any gaps in the price movement. Average true range atr atr is the average of true ranges over the specified period.

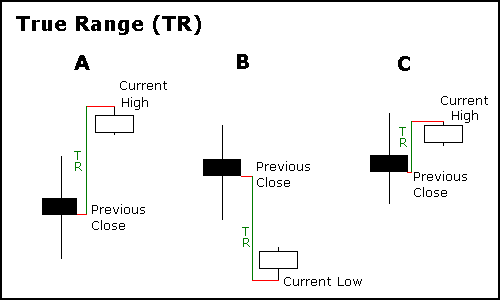

To form the beginning the first true range value is calculated as the high minus the low. Description average true range percent atrp expresses the average true range atr indicator as a percentage of a bar s closing price. The 14 day atr is the average of the daily true range values for the last 14 days.

How To Download Install Atr Indicator For Mt4 And Mt5

Scalping Forex Scalpingforex Forex Forex Trading System Binary

Choppiness Index Indicator Trading Strategy Stockmaniacs Trading Strategies Cryptocurrency Trading Trend Trading

Make 98 Profit Only In 30 Seconds Too Good To Be True With This Website You Can Trade And Make Easy Mercado De Acoes Investimento Investimento Financeiro

Monitoring Of Multiple Markets Timetotrade Community How To Get Rich Intraday Trading Online Trading

9qhdpc 41lowrm

Square The Range Trading System By Michael S Jenkins Sacred Traders Jenkins Trading System

Tiw8i54tv3y69m

S6k2u2mvvws6am

9tppj04maqj3km

S Viuxhhpoytgm

Doublecci Woodies Metatrader 4 Forex Indicator Forex Woodies Chart

My2 Nkyxrgutlm